A stock that has returned 95% over the past year and 122% year to date will attract attention. What it also attracts is the harder question: is any of that return justified by fundamentals, or is Arm Holdings simply riding a wave of AI enthusiasm that could reverse just as quickly?

I want to answer that question honestly, using the actual numbers rather than the narrative.

ARM Holdings Valuation 2026: The Numbers That Should Give You Pause

Let us start with what the market is paying for Arm Holdings right now.

At $255.27 per share, ARM carries a market cap of $271.6 billion and an enterprise value of $268.4 billion. Against trailing twelve-month revenue of $4.92 billion, that puts the EV/Revenue multiple at 47.6 times. The price-to-sales ratio is 55.25 times. The trailing P/E is 300.59 times. Even the forward P/E, which accounts for expected earnings improvement, comes in at 83.63 times.

To put those numbers in context, the average mature technology company trades at somewhere between 20 and 30 times forward earnings. High-growth companies might command 40 to 60 times forward earnings if growth is exceptional. ARM at 83 times forward earnings sits well above even the upper end of that range.

This is not automatically a reason to sell. Premium multiples exist for a reason, and ARM has earned some of its premium. But it does mean the stock is priced for perfection. Any slip in revenue growth, margin compression, or guidance cut could compress that multiple significantly and rapidly.

The EV/EBITDA of 203.88 times is particularly striking. For context, most valuation analysts flag anything above 25 to 30 times EBITDA as expensive. At 203 times, the company is trading on a projection of dramatically higher future earnings rather than anything close to current operating reality.

ARM Fair Value Estimate: What Is the Stock Actually Worth?

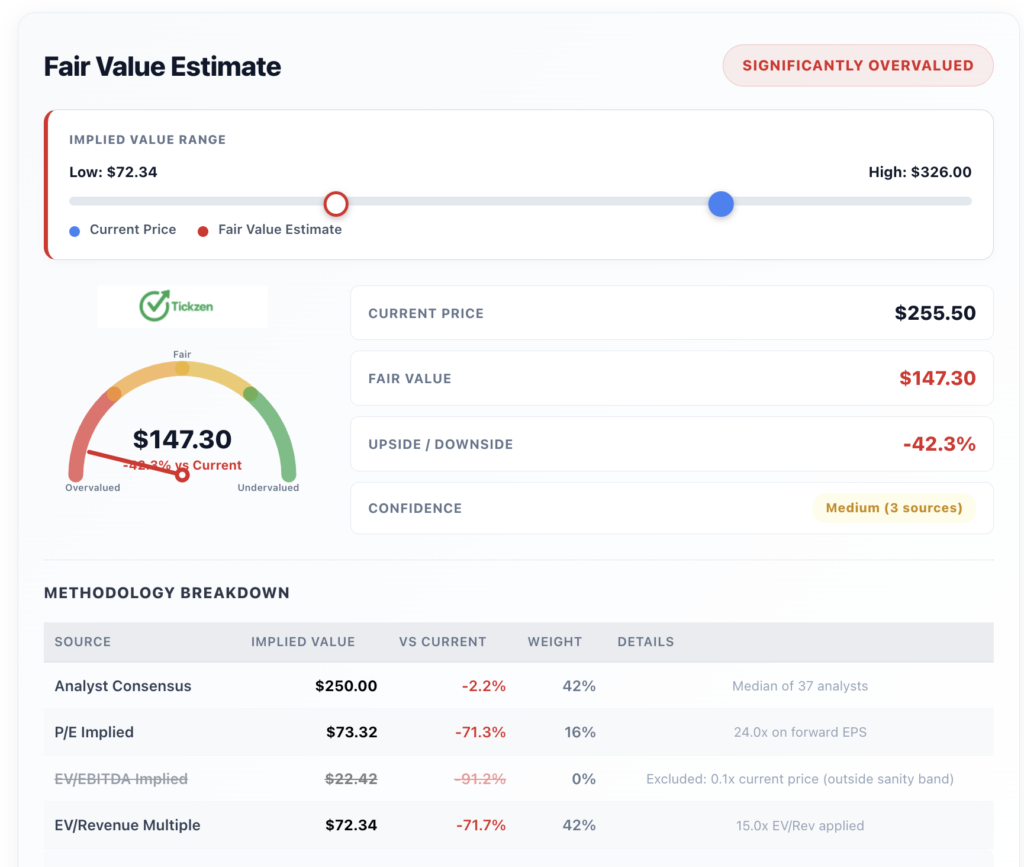

A blended fair value estimate using multiple methodologies puts ARM’s intrinsic value at approximately $147.30 per share, compared to the current price of $255.27. That implies roughly 42% downside from current levels to fair value.

Breaking down how that estimate is constructed makes the picture clearer.

Analyst consensus from 37 Wall Street analysts implies a value of $250, receiving a 42% weight in the blend. That is the most favorable input. The P/E implied value, using a sector-normalized 24 times multiple on forward earnings, produces a target of $73.32. The EV/Revenue implied value, applying a 15 times revenue multiple, yields $72.34.

The EV/EBITDA implied value was excluded from the calculation entirely because it fell below a reasonable sanity threshold, which itself tells you something about how stretched that particular metric is.

The wide range of outcomes between $72 and $326 tells you this stock is genuinely difficult to value. It is not that analysts are incompetent. It is that the business is transitioning and growing faster than traditional valuation frameworks can cleanly handle.

Still, a median analyst target of $250 and a fair value estimate of $147 while the stock trades at $255 should make any buyer think carefully about entry timing.

ARM Holdings Financial Health: Strong Business, Premium Price

The underlying business is genuinely solid, and this is important to separate from the valuation discussion.

Gross margin came in at 97.54% for the trailing twelve months. That is not a typo. ARM is primarily a licensing and IP business, which means its cost of revenue is minimal relative to what it charges. Operating margin is 29.60%, and net profit margin is 18.37%.

Revenue grew 20.1% year over year in the most recent quarter, with the latest quarterly revenue hitting $1.24 billion, up 9.4% sequentially. Earnings growth came in at 45.7% year over year. These are not the numbers of a struggling company.

The balance sheet is clean in most respects. ARM holds $3.6 billion in cash against $432 million in total debt. The current ratio is 6.0 times and the quick ratio is 5.65 times, signaling very strong short-term liquidity. The Altman Z-Score of 31.13 puts the company firmly in the safe zone with minimal bankruptcy risk.

Return on Invested Capital (ROIC) is 13.22%, which is respectable. Return on Equity is 11.95% and Return on Assets is 5.73%. These are decent numbers but not exceptional given the risk premium the stock commands.

The one area of concern is levered free cash flow, which came in at negative $281.5 million for the trailing twelve months. Operating cash flow is positive at $1.52 billion, but capital expenditures are consuming more than that when leverage is factored in. This is worth watching as AI infrastructure spending continues to intensify across the semiconductor sector.

More From Tickzen:

- Delta Air Lines Stock Analysis 2026: Is DAL Stock a Good Investment Right Now?

- Micron Technology Stock in 2026: Is MU Stock a Good Buy Right Now?

- Is IREN Stock Overvalued at $61? What the Numbers Say Before You Buy

- EchoStar SATS Stock Analysis 2026: Is the 7x Rally Running Out of Steam?

- MRAM Stock Up 172% in 15 Days — Is Everspin Technologies Still Worth Buying?

ARM Holdings Risk Factors Investors Need to Understand

There are several risks that the current stock price does not appear to be fully discounting.

The most immediate is regulatory. Earlier this month, ARM filed a $3.06 billion shelf registration for employee share plans while simultaneously coming under formal FTC antitrust investigation into its chip licensing practices. A formal antitrust action in the US, layered on top of regulatory scrutiny in South Korea, introduces meaningful uncertainty around the core licensing model that generates most of ARM’s revenue.

Valuation risk is the second major concern. At 83.6 times forward earnings, even a modest miss on guidance could produce a severe de-rating. The market has built in an assumption of sustained above-average growth. Companies with that kind of pricing embedded in their shares have very little margin for error.

Customer concentration adds another layer. ARM’s revenue depends on a relatively small number of large semiconductor companies and OEMs. If one or two large customers reduce orders, renegotiate royalty terms, or develop competing in-house solutions, the revenue impact would be disproportionate.

Competition from hyperscalers is a longer-term but growing concern. Amazon, Google, and Microsoft are all investing in custom silicon designs, some of which use ARM architecture and some of which do not. The more they move toward proprietary designs, the more pressure that places on ARM’s royalty revenue trajectory.

Capital expenditure intensity is also rising across the semiconductor industry. ARM is not a fab company, so it does not bear manufacturing capex directly, but its customers do. Supply constraints, allocation delays, and pricing volatility among chip manufacturers all create indirect risk for ARM’s growth plans.

ARM Semiconductor Stock Long-Term Outlook: The Case for and Against

The case for ARM over a long horizon is legitimate. The company’s instruction set architecture runs in an estimated 95% of the world’s smartphones. Its expanding presence in automotive chips, data center CPUs, and AI accelerators positions it well for the next decade of computing growth. Royalty revenue compounds naturally as ARM-based chips proliferate.

The case against ARM at current prices is simply about math. You are paying 47 times revenue for a company growing at 20% per year. Even if that growth rate is sustained for five years, the stock needs to either grow into the valuation or see its multiple compress. Multiple compression at these levels would be painful even against strong underlying revenue growth.

The upcoming July 29, 2026 earnings report is the next major inflection point. A beat with strong guidance would likely push the stock toward or above its 52-week high of $259.44. A miss, or any softening in the licensing revenue outlook, would test whether support at $206 actually holds.

For investors with a three to five year horizon who did not buy in the past six months, the current valuation likely makes more sense. For anyone considering a new position today at $255, the honest answer is that there are better entry points ahead unless the business materially exceeds current expectations in July.

Strong companies at stretched valuations still correct. ARM is a strong company. That does not make $255 the right price.

This article is for informational purposes only and does not constitute investment advice. All data referenced is sourced from public filings and market data as of May 20, 2026. Consult a qualified financial advisor before making investment decisions.