Snowflake stock jumped nearly 37% in after-hours trading on May 27, 2026. One quarter, one massive move. The question investors are now sitting with is whether that surge has already priced in the good news or whether this is the start of something bigger.

This SNOW stock analysis tries to cut through the noise with the actual numbers.

The Earnings Were Genuinely Strong

Snowflake reported Q1 FY2027 revenue of 1.28 billion dollars, up 34% year over year. That is not a rounding error. For a company already at scale, accelerating revenue growth is the single best thing management could show the market.

Free cash flow came in at 760 million dollars for the quarter. Gross margin held at 66.8%. These are not the numbers of a company struggling to find its footing. The Snowflake AI data cloud narrative is no longer just a slide deck story. Cortex Code and Snowflake Intelligence are driving real consumption growth from existing customers, and that matters more than new logo counts at this stage.

The company also raised its full-year FY27 guidance and announced a significant AI partnership with Amazon. If you have been asking is SNOW worth buying, the fundamental momentum case is stronger today than it was six months ago.

The Valuation Is the Honest Problem

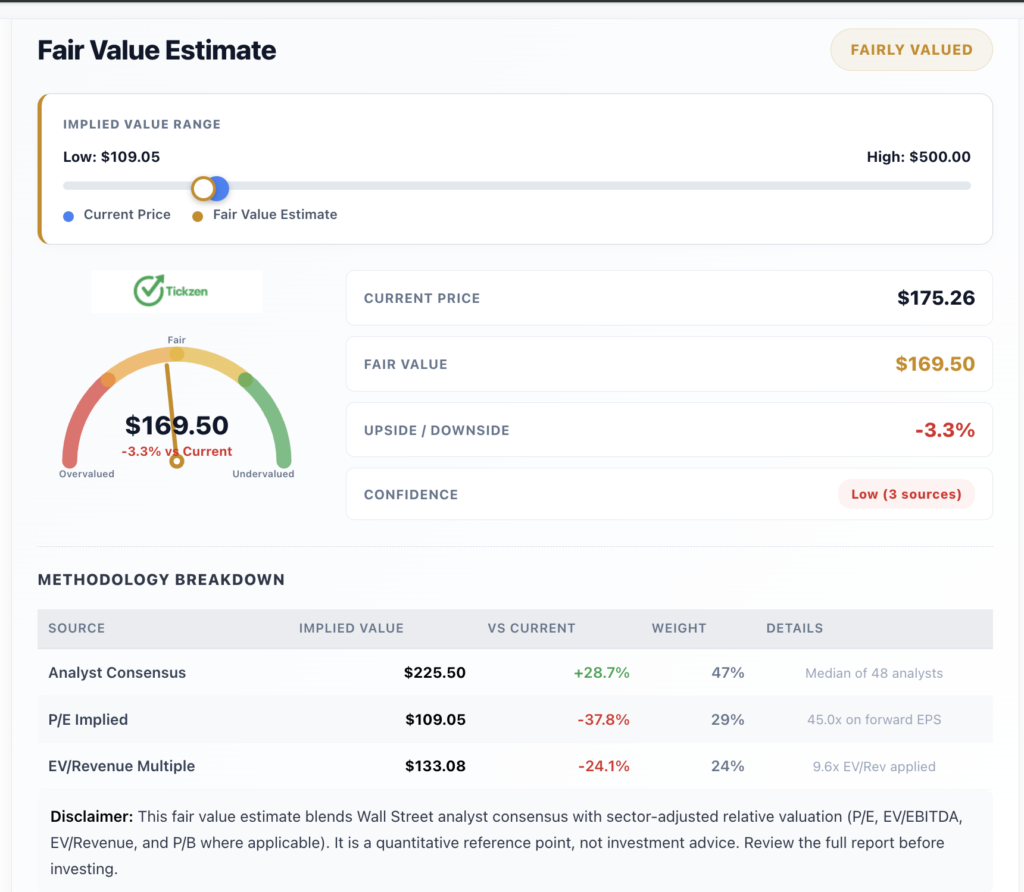

Now the uncomfortable part. Snowflake stock is trading at a forward P/E of 72.3x and a price-to-sales ratio of nearly 13x. The fair value estimate from a blended model of analyst consensus, P/E implied value, and EV/revenue sits at roughly 169.50 dollars. The current price is 175.26 dollars.

That means the stock is not cheap. It is priced for perfection, which is a different statement than it being a bad company.

The 48-analyst consensus target of 229.14 dollars implies 30.7% upside from here. That is a meaningful gap. But those same analysts are pricing in continued 30% revenue growth and an eventual path to profitability. The company is still burning roughly 28 dollars for every 100 dollars of revenue. Operating margins are negative 33%. These are not numbers you can ignore when the stock trades at a 12.6x EV/Revenue multiple.

This is the core tension in any SNOW stock analysis right now. Momentum points up. Fundamentals say the price assumes a lot of things going right.

More From Tickzen:

- AAL Stock Before Earnings: Can the July 2026 Report Finally Close the $15 Gap to Fair Value

- American Airlines Stock (AAL) Technical Analysis 2026

- Is IREN Stock Overvalued at $61? What the Numbers Say Before You Buy

- EchoStar SATS Stock Analysis 2026: Is the 7x Rally Running Out of Steam?

- Nokia Stock Technical Analysis 2026: Is NOK Overbought or Setting Up for the Next Big Move?

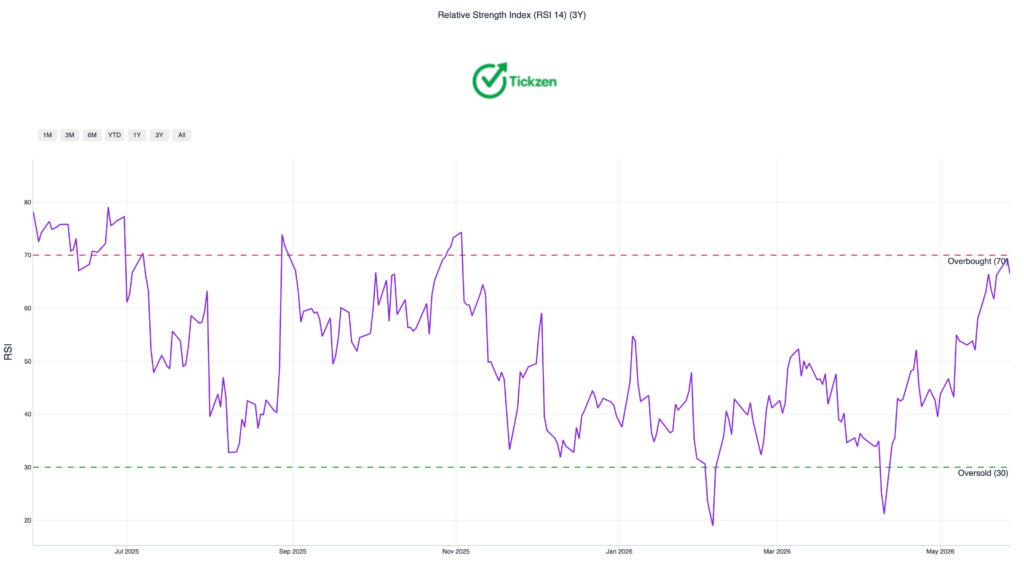

What the Chart Actually Says

The SNOW technical analysis picture is mixed, which is the honest read. The stock is above its 50-day moving average of 153 dollars. It is still below the 200-day moving average of 202.49 dollars. That gap matters because long-term trend followers will not turn fully bullish until the 200-day is reclaimed.

RSI at 66.5 is elevated. Not overbought, but not a clean entry either. MACD is bullish, supporting short-term continuation. The nearest-expiry options market is pricing an implied move of plus or minus 19.1% by June 26, which reflects how much uncertainty the market is still attaching to this stock. Implied volatility sits at 85.5%, ranking at the top of its 52-week range.

If you are looking at SNOW stock from a technical standpoint, the 163.36 dollar level is the line to watch. A close below it changes the short-term thesis. A sustained break above 180.77 dollars with volume would confirm the next leg up.

The SNOW Stock Outlook

Snowflake stock is not a broken business. Revenue is accelerating. The Snowflake AI data cloud product is gaining traction with large enterprise clients. Free cash flow is positive and growing. The balance sheet holds 4.03 billion dollars in cash against 2.74 billion dollars in debt.

The risk is not the business. The risk is the price you are paying for the business.

At 72x forward earnings, Snowflake needs to deliver 30%-plus revenue growth for the next three to four years while simultaneously closing the gap between gross profit and net income. That is achievable, but it requires flawless execution in an environment where enterprise technology budgets are under pressure.

Investors with a two-year-plus time horizon and high risk tolerance have a reasonable thesis. Short-term traders are buying into a stock that already moved 37% overnight, with historical volatility at 49% and a maximum drawdown history of 73%.

The SNOW stock analysis verdict: the business earned its reaction. The stock now needs the business to keep earning it.

This article is for informational purposes only and does not constitute investment advice. Always conduct your own research before making investment decisions.