Most coverage of EchoStar Corporation right now is written in one of two modes. Either it is breathlessly bullish about the FCC approvals and the $40 billion spectrum deals, or it is flatly bearish because of the $29.24 billion debt load and the negative net margin. Neither framing is particularly useful to someone trying to make an actual investment decision.

The reality of SATS stock in 2026 is messier, and more interesting, than either camp admits.

The Spectrum Deal That Changed Everything for EchoStar Stock

In May 2026, federal regulators cleared two major transactions allowing EchoStar to transfer a significant block of its spectrum holdings to SpaceX and AT&T. According to FCC filings reported by Benzinga, these deals together represent more than $40 billion in deal value.

For a company sitting on $29.24 billion in debt and running negative operating cash flow of $67.84 million over the trailing twelve months, the word “transformative” is not an overstatement. Spectrum is not a depreciating asset. It is a finite, government-controlled resource, and EchoStar had accumulated a substantial position through its legacy DISH satellite business.

The approval removed what analysts described as the final regulatory barrier to completing both sales. The stock gained significantly on the news, and if you look at the trading data, you can see the moment of impact. On May 13, 2026, SATS traded 8.13 million shares, nearly twice the daily average, and closed at $133.23.

What these deals do for the balance sheet, and what they do for the company’s operating trajectory, are two different questions. The proceeds need to go somewhere. Debt repayment would improve the financial health picture materially. A debt-to-equity ratio of 5.15x is not sustainable in a high-rate environment, and the market knows it.

Understanding the SATS Short Interest Squeeze Setup

With 36.17% of the float sold short, EchoStar is one of the more heavily shorted stocks in the Telecom Services sector. Short interest grew from 33 million to 41 million shares between March and April 2026, a 24% increase in a single month.

There are two reasonable interpretations of that data. The first is that informed market participants see the fundamentals as genuinely broken and believe the stock’s recovery is borrowed time. The second is that the spectrum deal rally attracted opportunistic short sellers who expected the news-driven momentum to fade quickly.

The days-to-cover ratio of 6.7x means that at average daily volume, it would take about a week for all short positions to be covered. That is not a squeeze setup in the way that certain retail-driven stocks have experienced, but it is enough to create sharp upside moves on positive catalysts. The FCC approval was exactly that kind of catalyst.

For investors watching SATS, the short interest dynamic is worth tracking monthly. A significant decrease in short interest following the spectrum deal news could indicate that the bears are capitulating. An increase, especially if the stock stays elevated, would suggest the short sellers believe the fundamentals have not actually improved despite the news flow.

EchoStar Debt and Financial Risk: Reading the Numbers Without Panic

The negative net income figure for SATS, which comes in at $14.44 billion for the trailing twelve months, looks catastrophic at first glance. Context matters here.

A loss of that magnitude in a single year for a company with $14.80 billion in revenue almost certainly includes a large non-cash charge, likely a goodwill impairment related to the legacy DISH subscriber base. The actual operating picture, while still concerning, is less dramatic. Operating margin is 8.91%. EBITDA margin is 10.72%. Gross margin is 27.08%.

What those margins tell you is that the core business, the part that involves running satellite and broadband infrastructure and serving customers, is not a money-losing operation. The problems are in the capital structure. Thirty billion dollars of debt, accumulated during the 5G spectrum acquisition phase and the Dish Network integration period, generates interest expense that overwhelms the operating income.

The current ratio of 0.30x and quick ratio of 0.24x are legitimate concerns. These numbers say that if EchoStar needed to meet its short-term obligations without new financing, it would struggle. The company is reliant on rolling over debt and maintaining credit facilities. In a normal market, that is manageable. In a credit crisis or significant rate shock, it becomes a serious problem.

The Altman Z-Score of -0.97 puts EchoStar in what financial models classify as the distress zone. That does not mean bankruptcy is imminent. Several major companies have spent extended periods in this zone while restructuring. But it does mean that the company has very little cushion for operational mistakes, and that the spectrum deal proceeds need to be deployed thoughtfully.

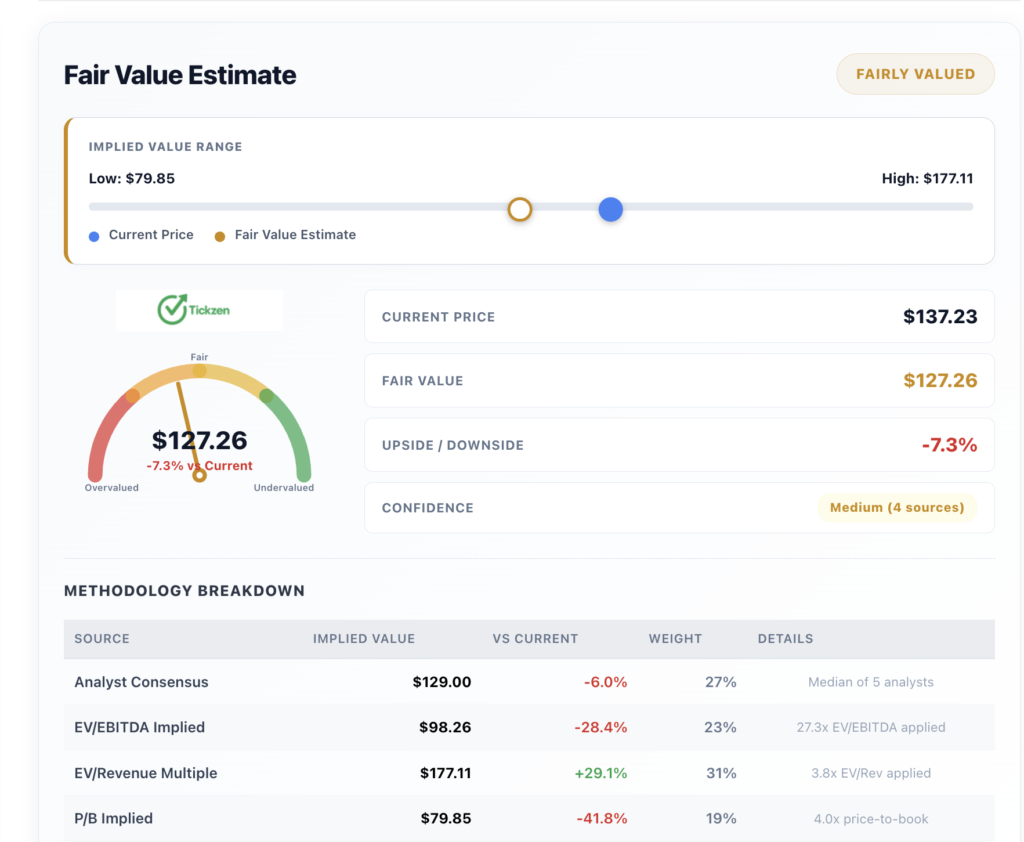

EchoStar SATS Valuation 2026: What Are You Actually Paying For?

At a price of $137.23 and an enterprise value of $49.47 billion, SATS trades at 4.56x revenue and 42.55x EBITDA. Neither multiple is cheap on its own. In the context of a company with declining revenue and negative free cash flow, they are a clear bet on future value, not present earnings.

The price-to-book ratio of 6.87x reflects the premium that satellite spectrum and wireless assets command relative to their book carrying value. The PEG ratio of 1.33x suggests the market is pricing in some growth recovery.

The fair value range in the current analysis spans from $79.85 on the low end (a book-value-anchored methodology) to $177.11 on the high end (an EV/Revenue multiple approach). The midpoint estimate is $127.26, which implies about 7.3% downside from the current price. Analyst consensus target is $129.60, implying -5.6% downside.

That analysts are rating the stock a Buy while setting targets below the current price tells you something specific: they believe in the direction of the company but think the stock has moved faster than the news warrants. Five analysts contributing to a consensus is a thin coverage base. The high target of $147.00 and low of $120.00 show meaningful disagreement about how to value the spectrum deal proceeds and the 5G network buildout timeline.

More From Tickzen:

- Delta Air Lines Stock Analysis 2026: Is DAL Stock a Good Investment Right Now?

- Micron Technology Stock in 2026: Is MU Stock a Good Buy Right Now?

- Is IREN Stock Overvalued at $61? What the Numbers Say Before You Buy

- EchoStar SATS Stock Analysis 2026: Is the 7x Rally Running Out of Steam?

- MRAM Stock Up 172% in 15 Days — Is Everspin Technologies Still Worth Buying?

EchoStar Business Segments: What Actually Generates Revenue

EchoStar is not a simple company. It runs four distinct operating segments, each at a different stage of maturity.

The Pay-TV segment handles the legacy DISH direct broadcast satellite business, including Sling TV and Freestream. This part of the business is contracting as subscribers move to streaming alternatives. That is why revenue is down 5.2% year over year.

The Wireless segment runs Boost Mobile and Gen Mobile. Boost Mobile is a meaningful asset, with a genuine subscriber base and a low-price positioning that competes directly with the major carriers in the prepaid market.

The Broadband and Satellite Services segment, operating under the Hughes and Hughesnet brands, serves rural homes, small businesses, and government and enterprise customers. This segment has historically been profitable and provides recurring revenue that is more stable than the pay-TV side.

The Other segment covers 5G network deployment. This is the part of the business that the spectrum deals enable, and it is also the part that has absorbed most of the capital investment over the past several years.

The combination of a declining legacy business, a growing but competitive wireless brand, a stable broadband business, and an early-stage 5G buildout is the actual EchoStar. The question for investors is which of those pieces the market will value most highly over the next two to three years.

SATS Stock Outlook: What Investors Should Watch Through 2026

The next scheduled earnings report is July 30, 2026. That report will be the first real opportunity to see whether the spectrum deal proceeds have had any impact on the balance sheet, and whether management provides updated guidance on the path to free cash flow.

Between now and then, watch three things. First, any updates on the actual closing timeline for the SpaceX and AT&T spectrum transactions. Regulatory approval was the last hurdle, but deals of this complexity take time to close. Second, Boost Mobile subscriber trends, which will indicate whether the wireless segment is gaining or losing ground in a competitive prepaid market. Third, short interest data for May and June, which will show whether the short sellers who grew their positions through April are covering or adding.

The 30-day historical volatility of 53.8% means that meaningful price swings in either direction are the norm, not the exception. Investors who are not comfortable seeing a 15% move in either direction in a single month should think carefully before sizing this position aggressively.

The FCC approval was real news. The spectrum asset value is real. The $29.24 billion debt is also real. All three things are true simultaneously, and the stock price at any given moment is the market’s best current guess about how they balance out.

Right now, that guess is $137.23.

This article is for informational purposes only and does not constitute financial or investment advice. All data sourced from public filings and financial analysis as of May 18, 2026. Always conduct your own research before making investment decisions.