How a 85-person semiconductor company is quietly becoming a critical piece of U.S. defense infrastructure.

There’s a pattern with small-cap semiconductor stocks. They operate in obscurity for years, serve genuinely important markets, and then one announcement flips the narrative entirely. Everspin Technologies (NASDAQ: MRAM) is going through exactly that right now — and while the 172% stock move in 15 days grabbed the headlines, the actual business development underneath is what deserves serious attention.

This isn’t just about a stock trade. It’s about a company with a real technology moat landing its first major defense contract — and what that might mean for the next three years.

The $40 Million Defense Contract: What It Actually Means

On April 30, 2026, Everspin Technologies announced a $40 million subcontract agreement with a U.S. prime defense contractor to supply Toggle MRAM process technology and engineering services for U.S. Defense Industrial Base customers. The contract runs 2.5 years.

To put that number in context: Everspin’s total TTM revenue is $55.2 million. This one contract is worth more than 72% of its annual revenue, spread across just 30 months. For a company with 85 employees, that’s transformational backlog.

What’s notable isn’t just the size — it’s the technology involved. Toggle MRAM (Magnetoresistive RAM) has specific properties that make it attractive for defense applications: it’s radiation-tolerant, it retains data without power (non-volatile), and it can withstand extreme temperature ranges. These aren’t features you bolt on after the fact. They’re intrinsic to the memory architecture, which means defense primes can’t easily swap in a competitor’s product once they’ve designed Everspin’s MRAM into a system.

That stickiness is worth thinking about seriously.

Everspin Technologies MRAM Manufacturing Expansion: The Microchip Technology Deal

Alongside the defense contract, Everspin announced a separate 10-year strategic manufacturing agreement with Microchip Technology to expand U.S.-based production capacity for MRAM and Tunnel Magnetoresistive (TMR) sensor products.

This deal is less flashy than the defense contract but arguably more important for the long-term MRAM stock investment thesis.

Here’s the problem Everspin has always faced: it doesn’t own a fab. Like most fabless or fab-lite semiconductor companies, it depends on foundry capacity. Partnering with Microchip Technology — a well-capitalized domestic semiconductor manufacturer — to secure dedicated U.S. production capacity addresses two concerns simultaneously: supply chain risk and the increasing regulatory preference for domestically sourced components in defense applications.

If you’re a defense prime contractor building systems for the U.S. military, “made in America” isn’t just a preference anymore — it’s increasingly a procurement requirement. Everspin just made itself a more eligible supplier.

Q1 2026 Earnings: Small But Meaningful Progress

The Q1 2026 results that came out alongside all this news were genuinely encouraging, even if they’re not spectacular on their own.

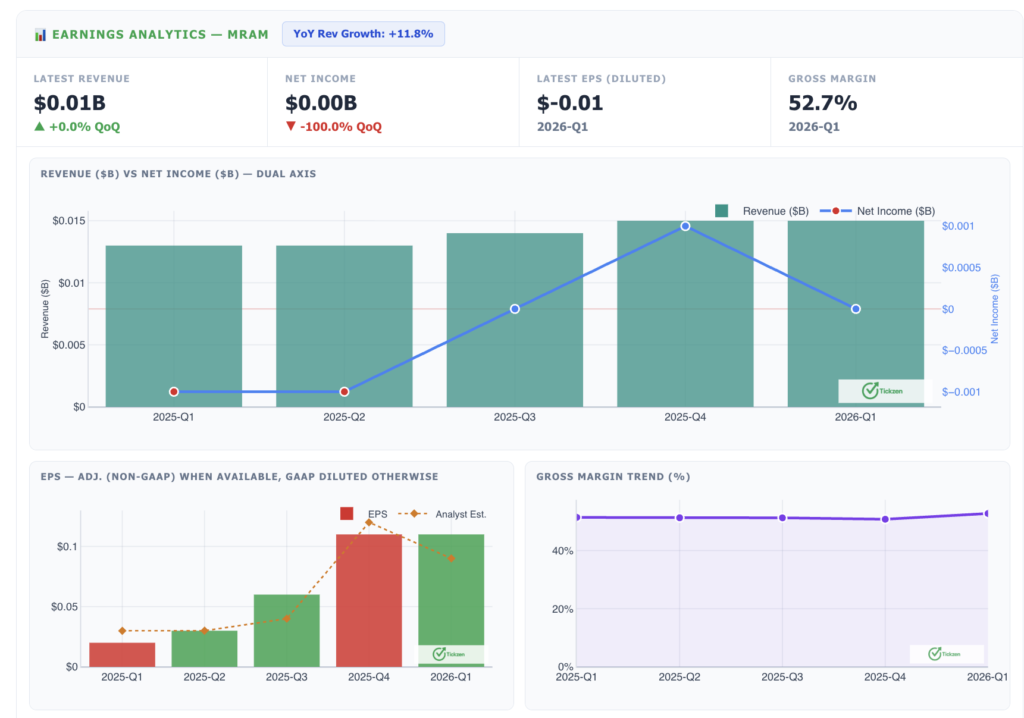

Revenue came in at $14.87 million, up from $13.14 million in Q1 2025 — an 11.8% YoY increase. Net loss narrowed to just $296,000. Gross margin improved to 52.7% for the quarter.

Q2 2026 guidance calls for $15.5–16.5 million in revenue, with a GAAP net loss per share of $0.12–$0.07. The midpoint of that range — roughly $16 million — would be another sequential improvement.

For a company that’s been working toward profitability for years, the trajectory here matters as much as the absolute numbers. Three consecutive quarters of revenue growth, narrowing losses, and now a $40 million contract backlog is a meaningfully different situation than where Everspin stood 12 months ago.

More From Tickzen:

- Delta Air Lines Stock Analysis 2026: Is DAL Stock a Good Investment Right Now?

- Micron Technology Stock in 2026: Is MU Stock a Good Buy Right Now?

- Is IREN Stock Overvalued at $61? What the Numbers Say Before You Buy

- Delta Air Lines Stock Valuation 2026: DCF Model, Fair Value, and the Hidden Risks Most Investors Miss

- Rocket Lab Stock Analysis 2026: Is RKLB Worth Buying at $105 or Is It Priced for Perfection?

MRAM Semiconductor Technology: The Competitive Moat Nobody Talks About

Everspin Technologies is the only company currently shipping MRAM at commercial scale. That’s been true for several years. It’s a strange position to be in — technically first to market with a superior memory technology that hasn’t yet had its breakout commercial moment.

MRAM combines the speed of SRAM, the density of DRAM, and the non-volatility of Flash. In theory, it should be eating into every one of those markets. In practice, the cost per bit remains higher than incumbent technologies, which has kept MRAM confined to applications where its unique properties justify the premium — industrial, medical, aerospace, and now defense at meaningful scale.

The defense contract is the clearest validation yet that for certain applications, Everspin’s MRAM is the right answer regardless of price. Defense programs don’t optimize for cost per bit the same way consumer electronics do. They optimize for reliability, radiation hardness, and supply chain integrity. On all three dimensions, Everspin’s Toggle MRAM scores well.

The company serves its products into industrial, medical, automotive/transportation, aerospace, and data center markets through direct sales and a network of distributors. The defense contract accelerates one of those channels dramatically while the Microchip manufacturing deal shores up the supply chain for all of them.

Financial Position: Healthy Enough for What Comes Next

The balance sheet gives Everspin room to execute without financial distress breathing down its neck.

The company holds $44.45 million in cash against just $3.34 million in debt — a genuinely strong net cash position for a small-cap semiconductor company. The Altman Z-Score of 9.54 puts it firmly in the financial “safe zone.” Current ratio of 4.84x means near-term liquidity isn’t a concern.

Operating cash flow for the trailing twelve months was $9.96 million — positive, which is the right direction. Levered free cash flow was $1.10 million, thin but positive.

The issue is that the company is still burning cash at the operating income level (-7.23% operating margin) because R&D and SG&A expenses are consuming most of the gross profit. With $28.24 million in gross profit against -$586K in net income, there’s a clear operational leverage story waiting to happen — if revenue continues growing, operating costs don’t scale proportionally, and the margin structure improves substantially.

That’s the bull case in plain terms.

The Risks: What Could Go Wrong for Everspin Technologies

This would be incomplete without an honest look at the risk side.

Execution risk is real. A $40 million contract is only as good as Everspin’s ability to deliver the engineering services and product volumes promised. For a company with 85 employees, scaling to meet defense program requirements is genuinely challenging. The Microchip manufacturing deal helps on the production side, but engineering capacity is a different constraint.

The stock price may have already priced in the good news. At $37.57, analysts have a mean price target of $18.00 — implying 52% downside. Those targets were set before the defense deal and may be revised upward, but even optimistic revisions would likely fall well short of $37.57. The forward P/E of 80.8x prices in profit growth that the income statement hasn’t delivered yet.

Customer concentration is a concern. The single $40 million defense contract makes up a large portion of backlog. If that program gets delayed, descoped, or cancelled (defense programs do all three), the revenue impact would be immediate and painful.

Short interest has increased. The number of shares sold short rose from 753K to 903K between March and April 2026, suggesting some institutional investors are hedging or outright betting against the stock even as it rallies.

The MRAM Stock Investment Case in Plain Terms

If you’re trying to assess whether Everspin Technologies belongs in a portfolio, here’s what you’re actually betting on:

You’re betting that the $40M defense contract is just the beginning of a larger relationship between Everspin’s MRAM technology and U.S. defense procurement. You’re betting that the Microchip Technology manufacturing deal lets Everspin scale production without supply chain disruption. And you’re betting that the 11.8% revenue growth rate accelerates as these deals convert to recognized revenue over the next 30 months.

That’s a credible thesis. It’s also a thesis that requires things to go reasonably well in a business that has historically had a long gap between technological capability and commercial scale.

Institutional investors agree with at least part of the story — 61.56% institutional ownership is meaningfully higher than you’d expect for a company this size. Smart money isn’t sprinting for the exits.

Whether $37.57 is the right price for that thesis is a different question. Based on analyst targets and fair value estimates that average around $17–18, the market is currently paying a significant premium for Everspin’s potential. That premium can persist — and even grow — if the next few quarters show continued improvement. But it also means there’s limited margin for error.

Watch Q2 2026 results closely. That’s when the first real data on whether the defense momentum is translating to the income statement will arrive.

This article is for informational purposes only and does not constitute investment advice. All data referenced is sourced from publicly available financial reports as of May 17, 2026. Consult a qualified financial advisor before making any investment decisions.